THIS

POST WAS ORIGINALLY PUBLISHED JUNE 17, 2007

Russian IPOs – Review of Week 24 of 2007

Investing in Russia – the Word Battle is Going On

Over

the past week there were a lot of discussions valuating the three-day

St. Petersburg International Economic Forum, RIA NOVOSTI reports that 8,966 people from 65 countries registered for the forum, with 9 presidents, 40 ministers, 40 ambassadors and luminaries such as James Wolfensohn, Yegor Gaidar and Francis Fukuyama in attendance. And the business outcome was rather impressive - contracts

worth $13.5 billion were signed between Russian and international

companies, including a deal between Aeroflot and Boeing. As the follow-on to the Forum, the Federal Statistics Service published this week a report on the Q1 2007. Russia’s economy expanded in the first quarter at the fastest pace in six years as production of building materials increased to keep pace with a construction boom and consumer demand remained strong. GDP rose at an annual rate of 7.9% in the period, compared with 5% Q1 2006. Industrial output increased 7.9% (4.1% in Q1 2006).

I posted earlier on the hot “Investments in Russia” issue, and here is some more to it. President Vladimir Putin had behind closed doors meeting with over 100 foreign business leaders. In his remarks the President called for investment into shipbuilding, aviation, high technology and other sectors. In general, many attendees of the Forum voiced positive commentaries, and I think that one of them is of an interested in a view of my previous posts - by Daniel Thorniley, Senior Vice President at the Economist Group: “Business in Russia is the best-kept secret in the world. More rubbish is written or spoken about Russia than any other country on earth.” He also accused the media (like The Wall Street Journal and CNN) of scaring foreign businessmen into thinking they will be murdered in Russian hotels and see their companies seized by the Russian mafia. A few days later a major article appears in the Newsweek International that says: “Russian President Vladimir Putin is in the world's doghouse because he does not appreciate sanctimonious lectures or missile batteries on his border. He and President George W. Bush patched things up a bit at the G8 summit last week, but the tension remains. Ironically, we as investors should be grateful. As a result of this alleged increase in political risk, the Russian stock market and its oil stocks in particular have been falling even as both emerging markets and energy equities have climbed. After a week in Russia, I am convinced there is no business reason for this stumble; it's all about the media rhetoric.”A very good illustration to all these discussions is the report on Neptune Russia & Greater Russia fund. Almost 90% of all analysts recently point to the “lackluster performance” of the Russian stock market since January this year. Neptune's Robin Geffen has a good commentary on this: he believes the current dip provides an excellent buying opportunity as proved to be the case a year ago. Mr. Geffen notes that the Russian markets often follow the pattern of a strong first quarter, a correction in the second, a consolidation period in the third and another stronger period at the end of the year. And this year that history is repeating itself. Another interesting feature is that Neptune Russia & Greater Russia fund shifted its focus to consumer sectors over a year ago and significantly reduced exposure to energy. The fund has maintained its consumer exposure and as at the end of April, it had 22.4% in consumer staples with 19.3% in energy, 16.6% in telecoms, 12.4% in materials, 9.6% in financials, 8.4% in utilities, 6.4% in cash, 4.8% in industrials and 0.1% in consumer discretionary. Mr. Geffen says: "The fund continues to benefit from the widespread misunderstanding of the Russian market. Historical perceptions of the Russian stock market being resource-led are no longer accurate."

I posted earlier on the hot “Investments in Russia” issue, and here is some more to it. President Vladimir Putin had behind closed doors meeting with over 100 foreign business leaders. In his remarks the President called for investment into shipbuilding, aviation, high technology and other sectors. In general, many attendees of the Forum voiced positive commentaries, and I think that one of them is of an interested in a view of my previous posts - by Daniel Thorniley, Senior Vice President at the Economist Group: “Business in Russia is the best-kept secret in the world. More rubbish is written or spoken about Russia than any other country on earth.” He also accused the media (like The Wall Street Journal and CNN) of scaring foreign businessmen into thinking they will be murdered in Russian hotels and see their companies seized by the Russian mafia. A few days later a major article appears in the Newsweek International that says: “Russian President Vladimir Putin is in the world's doghouse because he does not appreciate sanctimonious lectures or missile batteries on his border. He and President George W. Bush patched things up a bit at the G8 summit last week, but the tension remains. Ironically, we as investors should be grateful. As a result of this alleged increase in political risk, the Russian stock market and its oil stocks in particular have been falling even as both emerging markets and energy equities have climbed. After a week in Russia, I am convinced there is no business reason for this stumble; it's all about the media rhetoric.”A very good illustration to all these discussions is the report on Neptune Russia & Greater Russia fund. Almost 90% of all analysts recently point to the “lackluster performance” of the Russian stock market since January this year. Neptune's Robin Geffen has a good commentary on this: he believes the current dip provides an excellent buying opportunity as proved to be the case a year ago. Mr. Geffen notes that the Russian markets often follow the pattern of a strong first quarter, a correction in the second, a consolidation period in the third and another stronger period at the end of the year. And this year that history is repeating itself. Another interesting feature is that Neptune Russia & Greater Russia fund shifted its focus to consumer sectors over a year ago and significantly reduced exposure to energy. The fund has maintained its consumer exposure and as at the end of April, it had 22.4% in consumer staples with 19.3% in energy, 16.6% in telecoms, 12.4% in materials, 9.6% in financials, 8.4% in utilities, 6.4% in cash, 4.8% in industrials and 0.1% in consumer discretionary. Mr. Geffen says: "The fund continues to benefit from the widespread misunderstanding of the Russian market. Historical perceptions of the Russian stock market being resource-led are no longer accurate."

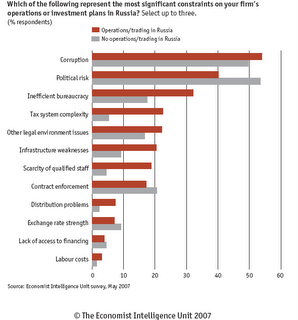

And of course, the major highlight of the past week is the survey, results of which are published by Clifford Chance law firm.

The Economist Intelligence Unit surveyed 455 executives around the

world in April 2007 about their perceptions of the challenges and

opportunities they face in doing business in Russia. Some 40% of the

respondents are based in Russia, and the remainder evenly split between

respondents from Asia-Pacific, North America and Europe. They come from a

wide range of industries, and approximately 65% of respondents

represent businesses with annual revenues of more than US$500m. You may

download the survey at the link, but I just want to pinpoint to some

results:

- When asked about the profit growth potential of the Russian market over the coming two-year period, 54% of respondents called it “high” or “very high”.

- When asked about the profit growth potential of the Russian market over the coming two-year period, 54% of respondents called it “high” or “very high”.

- In a number of areas, American firms appear significantly more sceptical than their global counterparts about the Russian market.

- There is money to be made in Russia: Respondents were very bullish about growth prospects, both in absolute terms and also relative to other major markets around the world.

And just one table. This shows the difference of views between operating and trading in Russia and those who are not.

- There is money to be made in Russia: Respondents were very bullish about growth prospects, both in absolute terms and also relative to other major markets around the world.

And just one table. This shows the difference of views between operating and trading in Russia and those who are not.

Vivid Illustration – US Chickens to Come to Russia

A U.S.-based supplier of broiler breeding stock and technical expertise for the chicken meat industry is in Russia. This week we learnt that after two years of extensive efforts to enter the poultry industry in Russia Cobb-Vantress is sending its first shipment of poultry breeding stock to the country. A new business alliance with Russian poultry distributor Broiler Budeshego (that is a subsidiary of the US firm Stromyn Breeders, LLC). "This is our first strong move to establish our brand of birds as a major breeding stock in the Russian market. Broiler Budeshego is a local Russian company who will widely distribute our stock throughout the country," said James Young, vice president of European and South American divisions of Cobb-Vantress. Budeshego is constructing a new farm and hatchery complex near Moscow and is expected to produce 2.5 million chickens initially, increasing to more than four million once in full operation, according to the Cobb-Vantress press release.

And More Prospects for InvestorsResearch and Markets published their Russia Food & Drink Report Q4 2006.

Russia’s broader consumer market is clearly booming. The report

significantly upgraded the total value estimate and forecast growth

scenario for the Russian mass grocery retail (MGR). The MGR market

should hit $17.45billion for full-year 2006, growing to $39.76 billion

by 2010, with an average compound annual growth rate (CAGR) of 23.3%

over five years. Local discount giant Magnit is gearing up for an IPO

and launching a trial run of a new supermarket chain to cater to

wealthier regional consumers. Emerging local players such as Lenta and

international firms Auchan and Metro are expanding in local markets as

well. The food sector is also prospering, with local players such as

leading food manufacturer, dairy and beverage producer Wimm-Bill-Dann,

restored to profitability growth in the large part due to booming

regional markets. Internationally-backed players, such as leading brewer

Baltika are benefiting from both regional growth and strong margins

driven by higher sales of premium brands. The report summarizes that

Russia offers massive growth potential through and well beyond 2010.

Newcomer to the Russian Banking Market

Every

week we learn about more and more foreign banks coming to Russia.

Earlier I mentioned about Barclays PLC. Now it is time for Chinese ICBC.

Some time ago the bank announced of its plans to extended operations in

Russia and focus on corporate banking. It applied for the license in

2005 and was expecting to start operations in 2006. Now it comes to 2007

reality – since February the recruiting campaign is under way. Everyone

remembers its biggest IPO of $ 22 billion last year. With its 355,000

employees worldwide the bank may easily start operations in Russia, but

many experts point to the fact that it is required at least three years

to roll out to full scale operations in Russia.

Investment Banking is on “War for Talent”

Related

to this new item is the issue of qualified personnel. I wrote quite a

while ago, that in order to operate efficiently in Russia any company,

banks including, needs to have a team that is nicely seasoned with

domestic personnel. And that is the question. Let us look at the latest

announcements and events. Of course this week everyone was stunned with

the news that JPMorgan Moscow allured the whole analytics team from MDM Bank, including its Head. This is a good illustration of what is called here in Moscow as “the war for talent”.

There is a huge deficit of experts in investment banking, primarily in

the top managers’ category. And it is increasing day by day. In March this year there had been 35 rotations in investment banks in Moscow – twice as much as compared to 2006. As an example Nicholas Jordan, co-head of Deutsche Bank's investment banking business in Russia, left in March after 11 years with the company to run Lehman Brothers Holdings Inc.'s new Moscow office. Expansions of business of the Russian firms plus announcements from Western banks add more fuel.

Goldman Sachs Group Inc., wants to add about 25 bankers to its Moscow office to keep pace with rivals including Morgan Stanley. Barclays PLC this year plans to open a Moscow office and “quickly'' expand it to 200 people. We may also remember banks from Japan, China, Cyprus, as well as plans for Toyota and Ford to open their banks. Of course each bank may bring its own staff to Russia, but they would definitely require local experts too. I personally was involved in this “the war for talent”. What I found out that most of the graduates of Russian prestigious financial colleges are already for 1-2 years employed by the Western financial institutions (and by the way, their salaries are very good for the students). And some of employees at my present company are being approached by the rival competitors too. But the issue of finding qualified staff will be hot for another 3-5 years. Young investment banking neophytes will take some time to mature. And it was illustrated by news this week. Kostroma’s Sovcombank and Novosibirsk-based ARKA Finance group, owned by Dutch TBIF BV, have set up a holding with $400 million in assets to develop retail banking in Russian regions. Market participants call it a good idea but add that it may work out not as fast as expected due to the lack of skilled employees in regions as well as in Moscow.

Goldman Sachs Group Inc., wants to add about 25 bankers to its Moscow office to keep pace with rivals including Morgan Stanley. Barclays PLC this year plans to open a Moscow office and “quickly'' expand it to 200 people. We may also remember banks from Japan, China, Cyprus, as well as plans for Toyota and Ford to open their banks. Of course each bank may bring its own staff to Russia, but they would definitely require local experts too. I personally was involved in this “the war for talent”. What I found out that most of the graduates of Russian prestigious financial colleges are already for 1-2 years employed by the Western financial institutions (and by the way, their salaries are very good for the students). And some of employees at my present company are being approached by the rival competitors too. But the issue of finding qualified staff will be hot for another 3-5 years. Young investment banking neophytes will take some time to mature. And it was illustrated by news this week. Kostroma’s Sovcombank and Novosibirsk-based ARKA Finance group, owned by Dutch TBIF BV, have set up a holding with $400 million in assets to develop retail banking in Russian regions. Market participants call it a good idea but add that it may work out not as fast as expected due to the lack of skilled employees in regions as well as in Moscow.